August 2023 - Week 2 Edition

Fitch Ratings Downgrades U.S. Treasury Debt

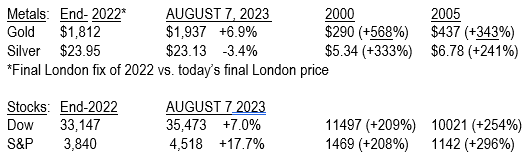

Gold is lower on Monday, August 7, mostly on expectations of slightly lower Consumer and Producer Price Inflation report to be released on Thursday and Friday – but inflation is a relatively small consideration in light of last week’s debt downgrade of U.S. Treasury securities by Fitch, a major credit rating agency. The stock market and gold fell a little, but the benchmark 10-year Treasury bond shot up to 4.20%, within 0.13% of its most recent peak of 4.33%, a reflection of greater U.S. credit risk.

America’s First Credit Downgrade Since 2011 Reflects Growing Biden-Era Deficits

Back in President Barack Obama’s first term, he ran up unprecedented trillion-dollar deficits every year from 2009 to 2012, fueling a spirited debt ceiling debate in August 2011 that eventually caused the first debt downgrade in U.S. history. That fueled a 20% decline in the S&P 500 and a 25% rise in gold prices, from $1,498 on June 27 to $1,878 on August 22. That obviously didn’t happen this time around, when Fitch & Co, downgraded U.S. credit for the second time in history last Tuesday, but the situation is perhaps more serious this time, since the numbers are so much higher than in 2011, and the Biden Administration does not take spending cuts with any sense of seriousness, much less the emergency attention they deserve.

On August 1, 2023, Fitch Ratings downgraded U.S. Treasury debt from AAA to AA+, due mostly to the U.S. government’s rapidly worsening financial conditions. Specifically, Fitch referred to “expected fiscal deterioration over the next three years” and an “erosion of governance… manifested in repeated debt limit stand-offs and last-minute resolutions.” When asked about the timing of the downgrade, Richard Francis, a senior director at Fitch, told Reuters that the agency had long-standing concerns about governance and the U.S. debt profile. Mark Sobel, a former longtime Treasury official agreed, saying, “Fitch isn’t telling anybody anything they don’t already know,” as “neither political party has evinced the guts to begin making the sacrifices needed on both the spending and revenue sides – which will only increase.”

Speaking of debt financing, the Treasury just announced it will need to auction $1 trillion in new Treasury instruments this quarter (July through September 30), up from $773 billion first expected. With Treasury rates ranging from 4.1% to 5.6%, that’s an average $48 billion in interest for each $1 trillion in debt and the debt is now $32 trillion ($1.5 trillion in interest) vs. under $15 trillion (at 1% rates, or $150 billion in interest) during the debt downgrade in 2011. The debt service numbers are 10-fold higher now.

So why did the stock and gold markets take last week’s debt downgrade so routinely, with a small (1%) Dow decline and no major move in gold? The only logical answer is that all the bad news was reflected where the rubber meets the road, in the sensitive Treasury bond market, where the 10-year Treasury rate soared up to 4.20% from 3.57% on June 1, and 3.74% as recently as July 18. On July 20, the non-partisan Congressional Budget Office projected some frightening deficit levels over the next 30 years:

“If current laws governing taxes and spending generally remained unchanged, the federal budget deficit would nearly double in relation to gross domestic product (GDP) over the next 30 years, driving up federal debt, the Congressional Budget Office projects. In CBO’s extended baseline projections, debt held by the public rises from 98 percent of GDP in 2023 to 181 percent of GDP in 2053.

“If, between 2023 and 2053, discretionary spending and revenues were at their 30-year historical averages as a percentage of GDP, then federal debt held by the public in 2053 would exceed 250 percent of GDP.”

Back in November 2010, there was a “Tea Party” revolt at the polls, resulting in an unprecedented 126-seat shift from a 63-seat Democrat majority in 2009-10 to a 63-seat Republican majority in 2011-12, which was a major cause of the robust debt-ceiling debate in August 2011 and the resulting debt downgrade, fueling gold’s rise to a then-record $1,900+ per ounce. In the mid-term election of 2022, however, there was no Republican rebellion, with just a 17-seat swing from a 7-seat Democrat edge to a 10-seat Republican majority and no overwhelming support for budget cuts in either Party. This is why we see trillion-dollar budget deficits every year in the foreseeable future, a crisis in the making.

What’s Ahead for Gold in the 2024 Election Year?

Right now, it looks like a repeat of the two aging and legally troubled candidates from 2020, Joe Biden and Donald Trump. Their legal (and Biden’s health) problems will dominate the debate instead of the all-important financial and geo-political challenges facing America, but it’s important to look back at similar times when high inflation and geo-political challenges like today’s wide array of potential problems faced us.

Let’s look at the Obama/Biden/Donald Trump years. The 2008 election was in the midst of a major financial crisis, as gold was rising in 2007 and 2008 while stocks were falling over 50%. Over the full year, gold beat stocks by a long shot, and gold was a clear winner in the last three election years.

We don’t know for certain who will run in 2024 but the problems facing America are more severe than at any time since World War II if you count the rapidly rising debt, weakened political, military and social structure at home vs. rising threats from Russia, China and Middle Eastern powers. We need a strong challenger with a backbone and – dare we hope – some fair major news organization press coverage! However, because The Washington Post editorial board has never endorsed a Republican since it began endorsing presidential candidates in 1976 and The New York Times has not endorsed a Republican presidential candidate since it endorsed Dwight Eisenhower in 1956, that is unlikely. It is for these, as well as, many other geopolitical and economic reasons, that I encourage you to regularly add gold and silver to your portfolio. Call us today and let our professional account representatives help you.

Metals Market Report Archive >

Important Disclosure Notification: All statements, opinions, pricing, and ideas herein are believed to be reliable, truthful and accurate to the best of the Publisher's knowledge at this time. They are not guaranteed in any way by anybody and are subject to change over time. The Publisher disclaims and is not liable for any claims or losses which may be incurred by third parties while relying on information published herein. Individuals should not look at this publication as giving finance or investment advice or information for their individual suitability. All readers are advised to independently verify all representations made herein or by its representatives for your individual suitability before making your investment or collecting decisions. Arbitration: This company strives to handle customer complaint issues directly with customer in an expeditious manner. In the event an amicable resolution cannot be reached, you agree to accept binding arbitration. Any dispute, controversy, claim or disagreement arising out of or relating to transactions between you and this company shall be resolved by binding arbitration pursuant to the Federal Arbitration Act and conducted in Beaumont, Jefferson County, Texas. It is understood that the parties waive any right to a jury trial. Judgment upon the award rendered by the Arbitrator may be entered in any court having jurisdiction thereof. Reproduction or quotation of this newsletter is prohibited without written permission of the Publisher.